Concept Of Materiality As A Constraint In Accounting

Pin By Mckell Kimball On The Accountant In Me Conceptual Framework Accounting And Finance Business Tax

Resultado De Imagem Para Accounting Principles Accounting Principles Accounting Accounting And Finance

Accounting Constraints Double Entry Bookkeeping

Pin By Paul Banting On Accounting Conceptual Framework Accounting Investing

The Structure Of The Conceptual Framework Of Accounting Google Search Conceptual Framework Framework Conceptual

Intermediate Accounting Ch 2 Diagram Quizlet

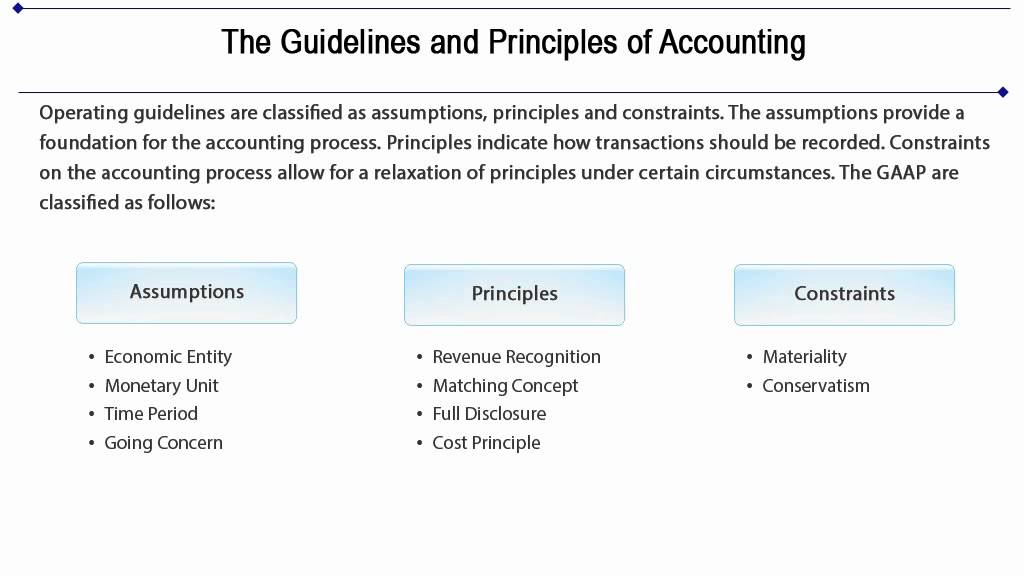

If a transaction is material enough to exceed the constraint threshold then it is recorded in the financial records and therefore appears in the financial statements if a transaction does not meet this threshold level it may not be recorded in the.

Concept of materiality as a constraint in accounting.

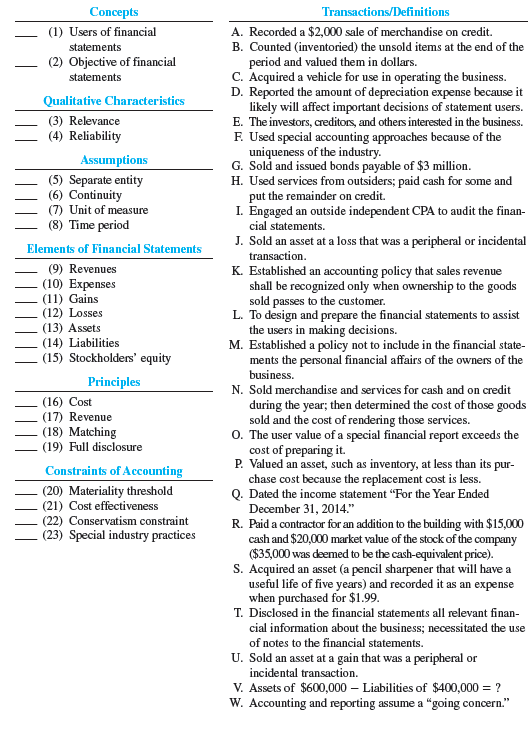

Solved Following Are The Concepts Of Accounting Covered In Cha Chegg Com

6 Constraints Of Accounting

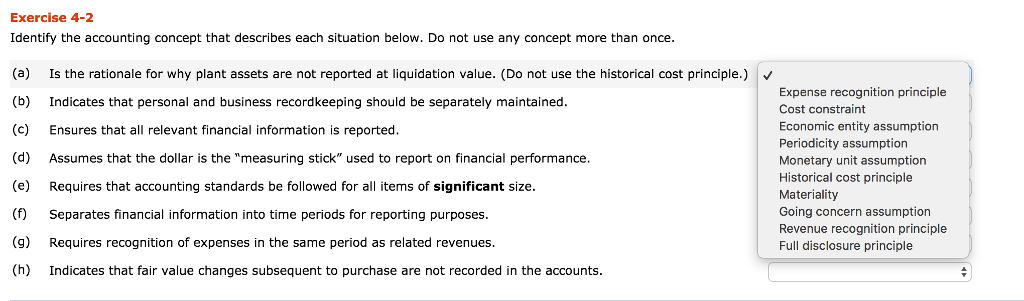

Solved Exercise 4 2 Identify The Accounting Concept That Chegg Com

Free Classifieds Ads Online Angels Ad Posting Website Accounting Online Online Ads

Accounting Principles Constraints Concepts And Assumptions By Billy Haps

Build A Simple To Do List App In Golang In 2020 Comprehension Activities Make A Donation To Do List

Top 19 Magento 2 Quote Extensions Free Medium Premium Options In 2020 Email Quotes Enabling Quotes Mass Quotes

الاطار النظري للمحاسبة Conceptual Framework Principles Equity

Accounting Principles Accounting Education Facebook

Accounting Principles Ppt Video Online Download

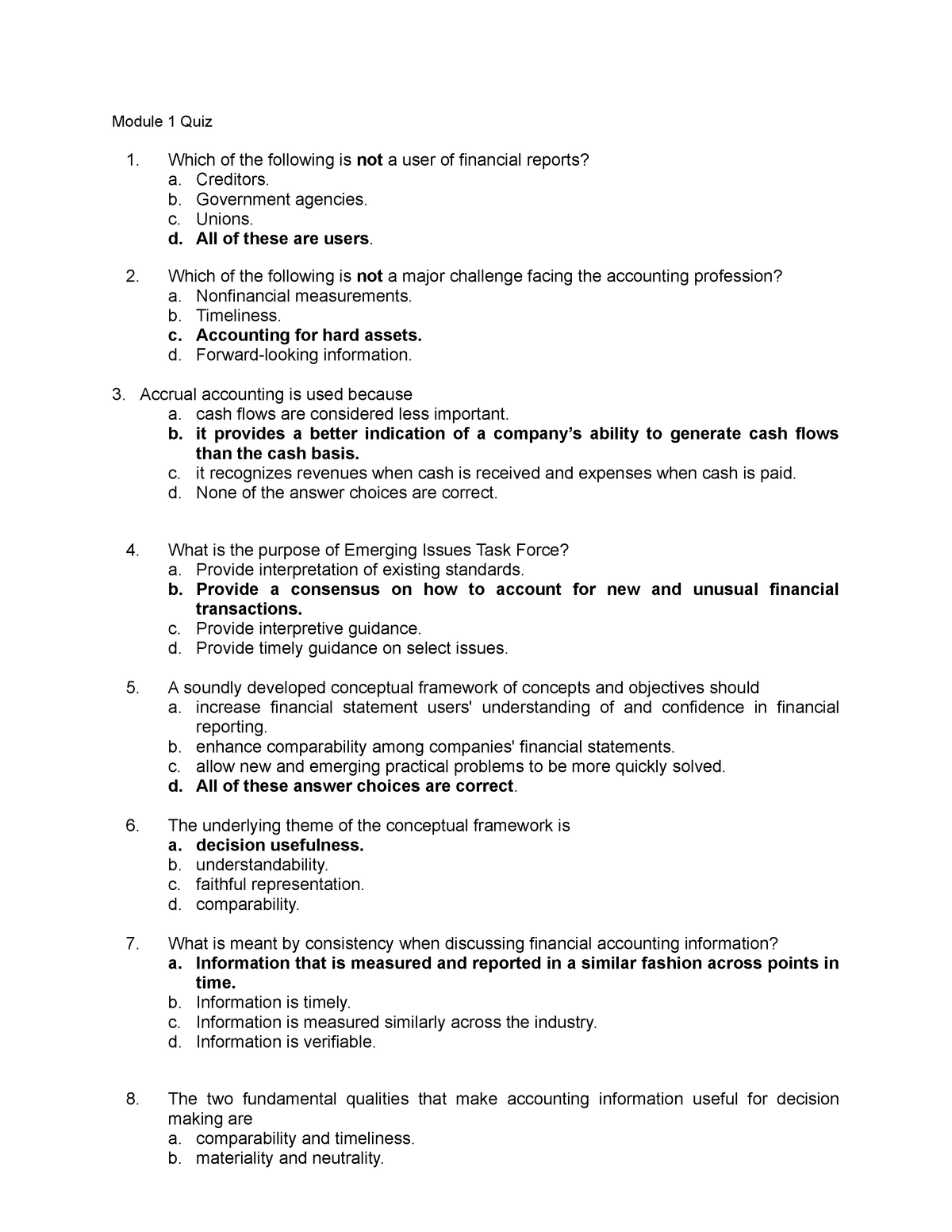

Quiz 1 Solution Acct 6306 Intermediate Accounting I Studocu

Framework For Management Accounting

Intermediate Accounting Ch 1

Image Accounting Concepts In A Diagram

Eyebrow Tutorial Eyebrow Tutorial Black Eyebrows Eyebrows

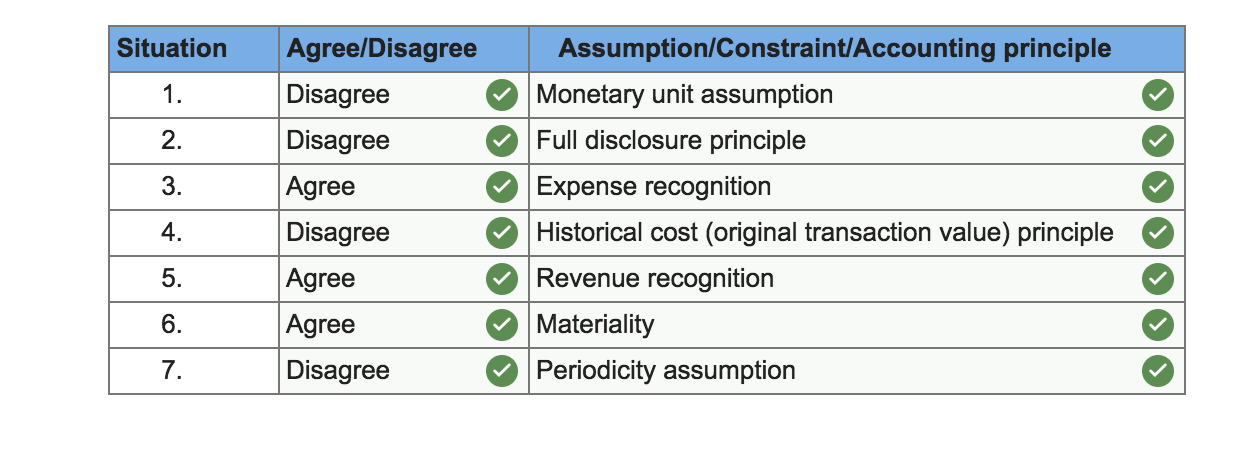

Listed Below Are Several Information Characteristics And Accounting Principles And Assumptions Match The Letter Of Each Homeworklib

Qualitative Characteristics Of Accounting Information Overview Guide

Does Getting An Mba Make Someone A Better Entrepreneur Financial Advisors Best Entrepreneurs Financial

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcslfdgw Wgx F0ckudemkuwqzsohv8bakbr4pjjnt7z9uwiteya Usqp Cau

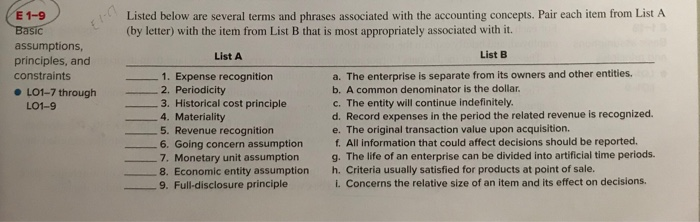

Solved Listed Below Are Several Terms And Phrases Associa Chegg Com

A Further Look At Financial Statements Financial Accounting Sixth Edition Ppt Download

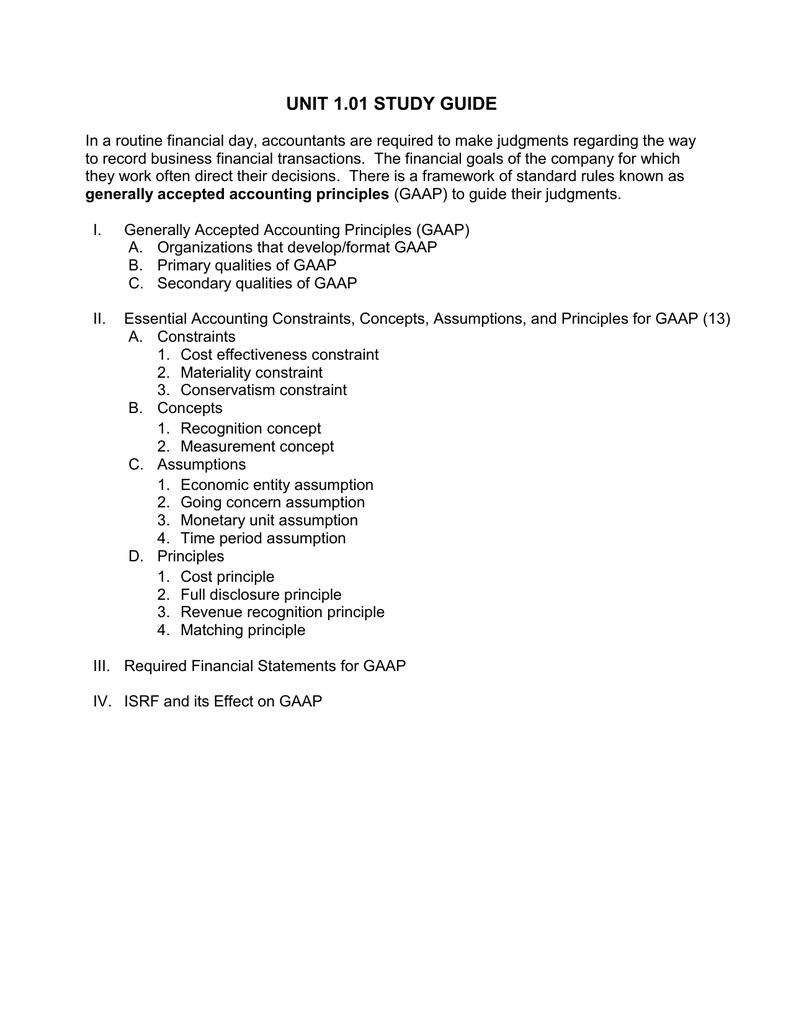

Unit 1 01 Study Guide

Accounting Principles Gaap Lessons Tes Teach

Before You Can Begin A Business As A Restricted Organization The Organization Itself Must Be Enlisted With Com Private Limited Company Private Company Company

Source : pinterest.com